Digital Net Worth Certificate vs Physical Copy – What’s Valid in 2026?

Welcome to our blog Digital Net Worth Certificate vs Physical Copy – What’s Valid in 2026? Net Worth Certificates (NWC) are important for loans, visas, trading accounts, and business purposes. With everything going digital, many people wonder if a digital certificate is enough or if they still need a physical copy. In 2026, both digital and physical certificates are legally valid. Digital certificates are fast, easy to share, and eco-friendly, while some banks and government offices may still prefer a physical copy. In this guide, we’ll explain which format works best, what the latest ICAI and RBI rules say, and tips to avoid mistakes so your certificate is accepted smoothly.

Understanding the Changing Format of Net Worth Certificates in 2026

Net Worth Certificates were traditionally issued as physical documents, signed and stamped by a Chartered Accountant (CA). These paper certificates were necessary for loans, visa applications, trading accounts, and other official purposes. But with the rise of digital processes, many CAs now issue Net Worth Certificates in digital PDF format. Digital certificates are faster to receive, easier to share, and can be stored securely without the risk of damage or loss. They also reduce paperwork, making the process more convenient for both individuals and institutions.

In 2026, digital NWCs are widely accepted as long as they are CA-certified and UDIN-verified. This verification ensures the authenticity of the certificate and compliance with ICAI and RBI guidelines. While physical copies are still required for certain regulatory submissions or specific banks, most financial institutions, lenders, and visa authorities now prefer digital certificates due to their convenience and speed. Using a digital certificate also allows for easy updates if your net worth changes, helping you stay compliant and ready for any financial or official requirement.

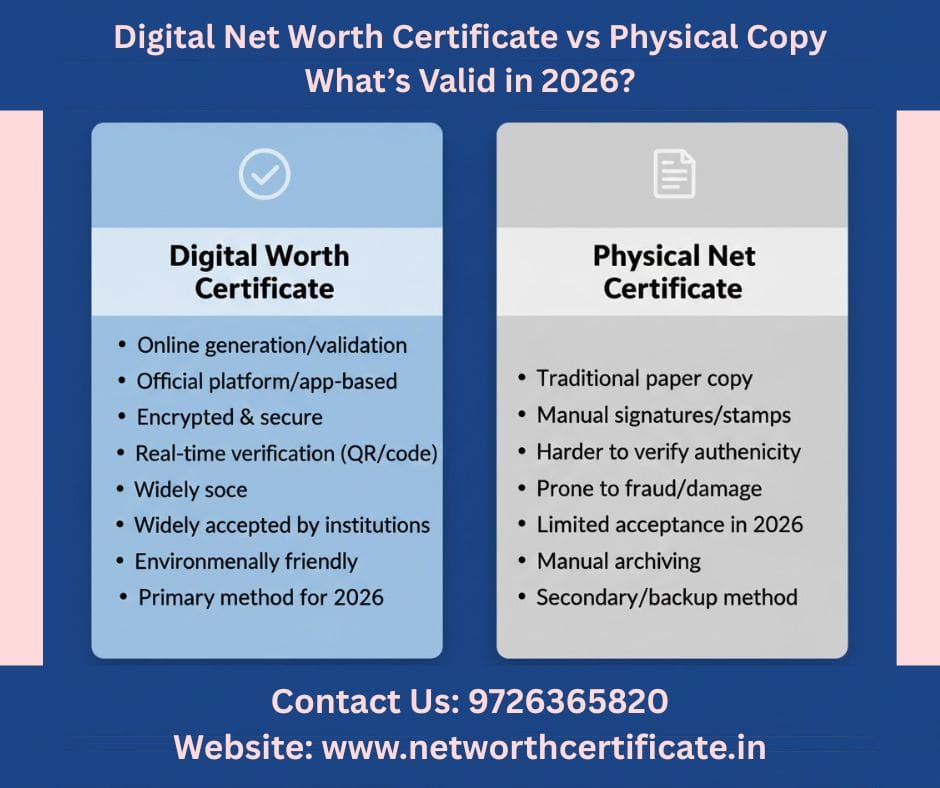

Key Differences Between Digital and Physical Net Worth Certificates

Digital and physical Net Worth Certificates both serve the same purpose, but they differ in speed, verification, security, and when they are accepted. Digital certificates are fast, easy to share, and can be verified online, while physical certificates provide traditional assurance and are still required in some official processes. The detailed comparison below will help you choose the right format.

| Feature | Digital Net Worth Certificate | Physical Net Worth Certificate |

|---|---|---|

| Format | PDF sent through email | Printed on CA letterhead with stamp and signature |

| Verification | UDIN-based online verification (real-time check) | Manual verification through stamp, seal, and signature |

| Processing Time | Instant to 24–48 hours | Longer due to printing, signing, and courier delays |

| Convenience | Very easy to share via email, WhatsApp, or online portals | Needs to be carried or couriered physically |

| Acceptance | Accepted by most banks, lenders, and visa authorities | Always accepted for government and regulatory submissions |

| Security | Protected with digital signatures, UDIN, and PDF locking options | Risk of tampering unless carefully checked |

| Risk of Loss/Damage | No risk — can be stored digitally and downloaded anytime | Can be misplaced, torn, or damaged |

| Storage | Easy to save on phone, email, or cloud | Needs physical filing and safe storage |

| Cost | Usually lower as no printing or courier is required | Slightly higher due to printing and dispatch costs |

| Best Use Case | For fast online submissions, bank loans, visa uploads | For government departments, physical document verification |

| Environment Friendly | Yes — paperless and eco-friendly | No — uses paper, printing, and courier resources |

| Editing/Corrections | Easy for CA to update & resend | New printout required for corrections |

Legal Validity of Digital and Physical Net Worth Certificates in 2026

In 2026, both digital and physical Net Worth Certificates are legally valid as long as they are issued by a Chartered Accountant and verified with a UDIN. Digital certificates are fully supported under the Information Technology Act, 2000, which gives legal recognition to electronic documents and digital signatures. Because of this, most banks, lenders, and visa authorities accept a PDF Net Worth Certificate just like a physical one, making the digital format faster and more convenient for online submissions.

However, certain regulatory bodies and government departments still prefer or require the original printed certificate. Submissions related to RBI compliance, as well as CDSL/NSDL depository forms, may ask for a physical copy with the CA’s stamp and handwritten signature. Since each institution follows its own rules, it’s always smart to check the required format in advance. This helps ensure your certificate is accepted without any delays or repeated submissions.

How Digital Certificates Are Authenticated and Verified (UDIN System) ?

Digital Net Worth Certificates are authenticated using a UDIN (Unique Document Identification Number) issued by the Chartered Accountant. This system ensures complete transparency and trust. With UDIN, institutions can:

Verify the CA’s identity and confirm that the certificate is genuinely issued by a registered professional.

Check online whether the certificate is original or has been tampered with.

Ensure full ICAI compliance, as UDIN is mandatory for all financial certificates.

Match the certificate details (name, date, and figures) with the UDIN database to avoid fraud.

Validate the certificate anytime, even after years, because UDIN records are stored securely.

Speed up processing, as banks and visa offices can instantly verify the document online.

Reduce dependency on physical copies, since UDIN gives digital certificates the same credibility as hard copies.

Why Physical Certificates Still Carry Legal Strength in 2026 ?

Even with the rise of digital documentation, physical Net Worth Certificates remain legally strong in 2026. A printed certificate includes the Chartered Accountant’s original signature, stamp, and seal, which many institutions still consider more reliable for formal or high-stakes verification. This gives physical certificates an edge in situations where authenticity needs to be unquestionable.

Certain submissions, such as regulatory compliance, stock market depository forms (CDSL/NSDL), and specific government applications, often require the original hard copy. While digital certificates are faster and convenient for most banks and online processes, physical certificates continue to provide traditional trust and legal assurance wherever original documents are necessary.

When to Use a Digital Certificate and When a Physical Copy Is Required

Deciding between a digital or physical Net Worth Certificate depends on what you need it for. Digital certificates are fast, easy to share, and perfect for most banks, loans, or visa applications. Physical certificates are better when original documents are required, such as for government, regulatory, or official submissions. Here’s a quick guide to help you choose:

| Use Case | Digital Certificate | Physical Certificate |

|---|---|---|

| Speed & Convenience | Quick processing for loans, visas, and bank applications | Slower, needs printing and courier delivery |

| Submission Format | Accepted if the institution allows PDF or scanned copies | Required when the original signed copy is needed |

| Storage & Sharing | Easy to save digitally and share online | Must be physically carried or sent by courier |

| Official/Legal Use | Good for most banks, lenders, and visa offices | Preferred for government, RBI, or depository submissions |

| Authenticity | Verified online via UDIN | Maximum legal trust with CA signature and stamp |

Latest ICAI & RBI Guidelines That Impact Certificate Format

As of 2026, the ICAI mandates that every Net Worth Certificate must include a UDIN (Unique Document Identification Number), whether issued digitally or in physical form. This ensures the certificate is genuine, tamper-proof, and fully compliant with professional standards. At the same time, RBI guidelines require CA-certified certificates for banks, NBFCs, and other financial institutions to process loans, credit approvals, and other regulatory submissions.

Key points to keep in mind:

Digital certificates with UDIN are legally valid and widely accepted by most banks, lenders, and visa authorities.

Physical certificates may still be required for regulatory filings, government submissions, or depository forms like CDSL/NSDL, where original documents are mandatory.

Always check the institution’s requirements before submitting your certificate to avoid delays or rejections.

Digital certificates save time, reduce paperwork, and are easy to share or store securely online.

Physical certificates provide traditional legal assurance and are often preferred in formal or high-value transactions.

Keeping a copy of both formats can be helpful: digital for fast submissions and physical for official or regulatory purposes.

Ensuring your certificate follows both ICAI and RBI guidelines protects you from compliance issues and strengthens trust with banks, investors, and authorities.

Common Submission Mistakes to Avoid in 2026

Submitting without UDIN: Always ensure your certificate has a valid UDIN, as institutions may reject certificates without it.

Sending unclear or tampered copies: Avoid submitting scanned or photographed copies that are blurry, incomplete, or altered in any way.

Assuming digital certificates are accepted everywhere: While most banks and lenders accept digital certificates, some regulatory or government submissions may still require the physical copy.

Delaying submission unnecessarily: Don’t wait for a physical certificate if a digital version is sufficient, as this can cause delays in loan approvals, visa applications, or other processes.

Ignoring institution-specific instructions: Always check the exact format, signature, and verification requirements before submitting to avoid rejection.

Providing outdated financial information: Make sure the certificate reflects your latest net worth to prevent discrepancies.

Not double-checking CA details: Verify the CA’s name, registration number, and contact information for accuracy.

Forgetting to retain copies: Keep both digital and physical copies for future reference or compliance needs.

Submitting incomplete documents: Ensure all required annexures, schedules, or supporting documents are attached.

Overlooking deadlines: Submit your certificate well before the institution’s cut-off date to avoid delays or penalties.

Get Expert Help for Your Net Worth Certificate in 2026

If you need your Net Worth Certificate prepared quickly and accurately, our experienced team is here to assist. We ensure your certificate is CA-certified, UDIN-verified, and fully compliant with ICAI and RBI guidelines. Whether you prefer a digital PDF for fast online submission or a physical copy for regulatory requirements, we handle everything efficiently so you can focus on your financial or official needs.

Our services include fast online documentation, precise net worth calculation, and issuance of a legally valid digital or physical certificate. With our support, you can avoid common mistakes, meet submission deadlines, and have peace of mind that your certificate will be accepted by banks, lenders, visa authorities, and regulatory bodies.

📞 Contact: +91 97263 65820

🌐 Website: https://networthcertificate.in/