Latest RBI Guidelines for Net Worth Certificate in Loans 2025–26

Welcome to our blog on the Latest RBI Guidelines for Net Worth Certificate in Loans 2025–26. If you’re planning to apply for a loan, whether as an individual or a business, a Net Worth Certificate (NWC) is a crucial document that banks and financial institutions rely on to assess your financial stability. The RBI has updated its rules for 2025–26 to ensure a standardized, transparent process, making it easier for applicants to comply and get their certificates approved quickly. In this guide, we’ll cover who needs a net worth certificate, the eligibility criteria, the documents required, and the charges involved. We’ll also explain common mistakes to avoid and how following these guidelines can streamline your loan approval process. By understanding the latest RBI norms, you can prepare all necessary documents in advance, save time, and ensure a smooth, hassle-free experience when applying for loans.

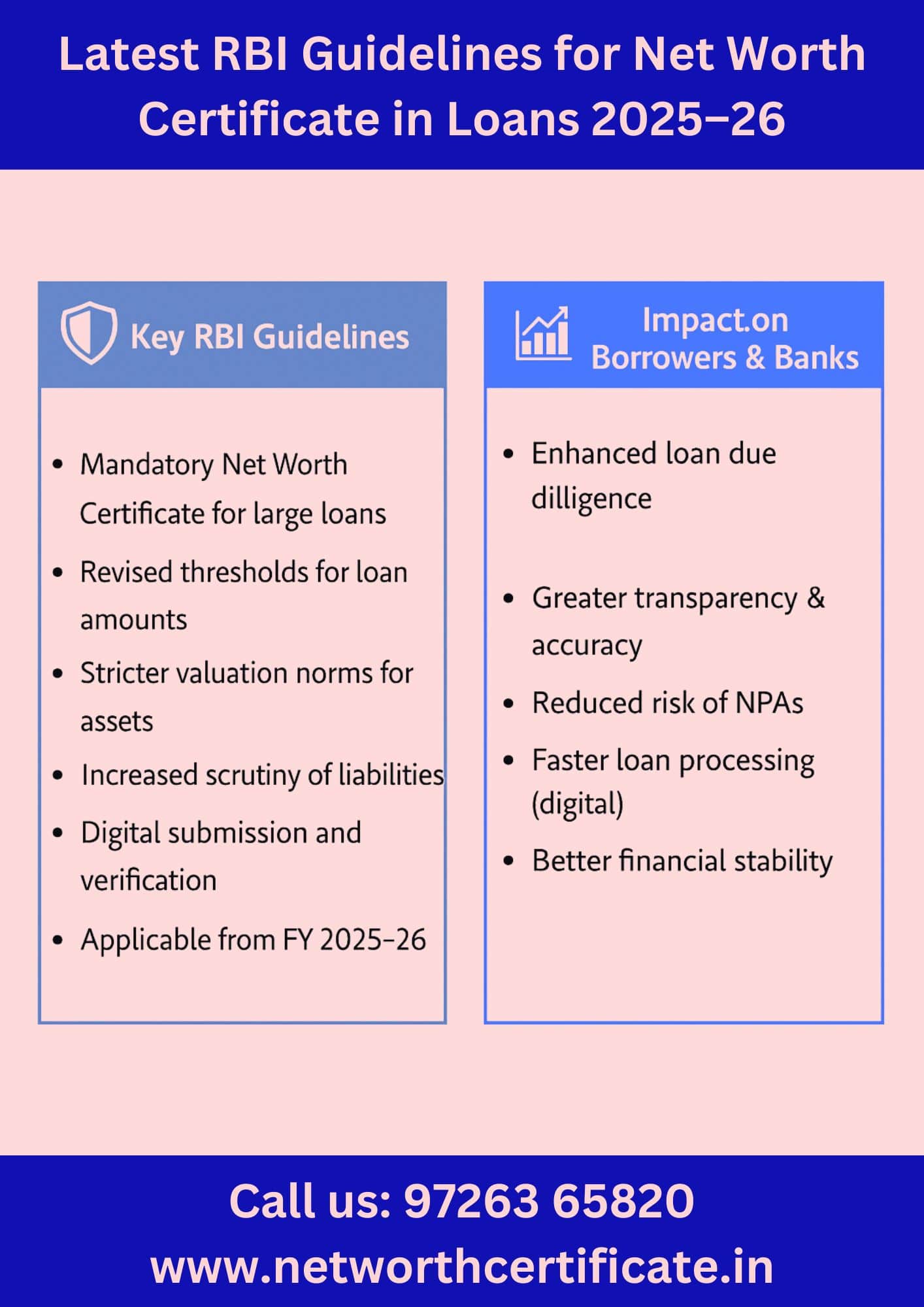

RBI Guidelines for Net Worth Certificate 2025–26

The latest guidelines followed by banks for 2025–26 make it clear that only a CA-certified Net Worth Certificate is acceptable during loan processing. The certificate must include a proper calculation of all your personal and business assets and liabilities, verified by a Chartered Accountant who issues it with a valid UDIN for authenticity. Banks rely on this UDIN to confirm that the certificate is genuine and issued by an authorized CA. Additionally, the certificate must follow ICAI’s standard format, including CA’s seal, signature, membership number, and the “as on date” of valuation. Most banks also insist that the certificate should be recent—preferably not older than 3 to 6 months—so they can assess your current financial strength without outdated numbers.

Apart from asset verification, all liabilities must be declared in full, including home loans, personal loans, business loans, credit card dues, overdrafts, and outstanding EMIs. Banks now place high importance on transparent reporting, and any hidden or undisclosed liability can raise doubts or delay loan approval. Many financial institutions also cross-check the figures with ITR, GST data, bank statements, and investment proofs to ensure accuracy and consistency. These updated guidelines ensure genuine valuation, reduce errors, and make the loan approval process smoother for applicants. By following these norms correctly, you can build trust with the bank, avoid re-verification, and speed up your overall loan approval process.

What is a Net Worth Certificate and Its Importance for Loans

✔️ A Net Worth Certificate (NWC) is a simple summary of your financial position, showing how much you truly own after subtracting all your outstanding loans and dues.

✔️ It is prepared and certified by a Chartered Accountant, who checks your bank balance, investments, property, gold, business capital, and all liabilities before issuing the certificate.

✔️ Banks depend on this certificate to understand whether you can comfortably repay the loan, especially when the loan amount is high.

✔️ A strong net worth increases your credibility, giving lenders confidence that you are financially stable and responsible.

✔️ The certificate helps banks decide loan limits, interest rates, and overall risk category for the applicant.

✔️ For business owners, an NWC helps show the true strength of the business, which is important for working capital loans, MSME loans, and expansion finance.

✔️ For individuals, it is useful for home loans, mortgage loans, and personal loans where financial background matters.

✔️ With RBI’s updated 2025–26 banking practices, banks now follow a more uniform and transparent process, making the certificate even more important for smooth loan approval.

✔️ An accurate NWC also prevents back-and-forth queries, saving time and helping your loan application move faster.

Who Needs a Net Worth Certificate for Loan Approval ?

🔹 Individuals applying for high-value loans like home loans, mortgage loans, or large personal loans where banks check overall financial stability.

🔹 Business owners, proprietors, and partners who need to show business strength for working capital, CC/OD limits, term loans, or machinery loans.

🔹 Companies, LLPs, and private firms applying for project financing, tenders, bank guarantees, or large credit limits.

🔹 Startups and new entrepreneurs applying for MSME loans, CGTMSE loans, PMEGP, Mudra loans, or SIDBI funding.

🔹 Persons applying for education loans or foreign visa documentation, where financial capacity must be proven.

🔹 Individuals purchasing commercial or residential property, where banks may ask for a complete financial profile beyond salary slips.

🔹 People with multiple income sources (salary + business + rental + investments) who need a consolidated financial summary.

🔹 Applicants going for loan restructuring or enhancement, where banks check improved net worth before increasing limits.

🔹 High net-worth individuals (HNIs) who require a financial statement for investment, wealth declaration, or compliance purposes.

🔹 Exporters/importers applying for credit limits under banking schemes where financial strength must be validated.

Eligibility Criteria for Individuals and Businesses

Your assets and liabilities should be properly documented and easy to verify.

A valid PAN card and ID proof must be submitted for verification.

Bank statements should match the balances you declare in your net worth details.

If you have loans, provide the latest loan statements or sanction letters.

The certificate must be issued only by a qualified, practicing Chartered Accountant.

Businesses should have properly audited financial statements for the relevant financial year.

Ownership and shareholding details of the business must be clear and updated.

Ensure there are no major mismatches between your financial documents.

Keep additional documents ready—your CA may request them if your finances are complex.

All documents should be recent, genuine, and free from errors to avoid delays.

Impact on Different Types of Loans

| Loan Type | How Net Worth Certificate Helps You |

|---|---|

| Personal Loan (High Amount) | Banks check your net worth to decide how much risk-free you are. Higher net worth = smoother approval + better chance of higher limit. |

| Business Loan / Working Capital | Helps lenders understand your business’s real financial strength. A strong net worth often leads to better interest rates and quick sanction. |

| MSME Loans | Many MSME schemes require proof of financial stability. A net worth certificate helps you qualify faster under credit guarantee schemes. |

| Startup Funding / Project Finance | Investors and banks assess promoter’s net worth before funding. It builds trust and shows your repayment capability. |

| Loan Against Property (LAP) | A solid net worth profile supports property valuation and improves your eligibility for bigger loan amounts. |

| Home Renovation / Construction Loans | Lenders use net worth to check your financial stability for long-term repayment. |

| Education Loan (High Value) | For large overseas education loans, banks verify the sponsor’s net worth to finalize loan approval. |

| Government Subsidy-Based Loans | Certain subsidy-based programs require financial verification through a CA-certified net worth certificate. |

| Overdraft / Cash Credit (CC) Limits | A higher net worth strengthens your case for increased CC limits and renewal approvals. |

| Import–Export / Trade Finance | Banks check net worth to ensure you can handle international trade risks and payments. |

Documents Required as per RBI Guidelines

To get a Net Worth Certificate under the latest RBI guidelines, you must provide clear proof of your assets, liabilities, and identity. These documents help the CA verify your financial position accurately and issue a certificate that banks can fully rely on.

PAN Card and Aadhaar Card (for individuals)

Latest audited financial statements (for companies/partners/proprietors)

Recent bank statements (savings/current)

Fixed deposit (FD) details and certificates

Property documents with valuation (if available)

Vehicle RC copies with current value

Investment proofs (Mutual Funds, Shares, LIC, PPF, NPS, Bonds, etc.)

Loan statements for home loan, personal loan, business loan or overdraft

Credit card outstanding statement (if applicable)

Business registration proof (GST, Partnership Deed, MOA/AOA, etc.)

Timeline and Validity of Net Worth Certificate

Net Worth Certificate is time-sensitive because banks always want your latest financial position. Since your assets and liabilities keep changing (new investments, EMIs, loans, income, etc.), lenders rely only on a recent and updated certificate to process any loan application smoothly.

Here’s how the timeline and validity work:

Validity is usually 6 months from the date the CA issues the certificate.

Some banks may ask for a new certificate if your finances have changed or if the loan amount is high.

For most loan applications (personal, business, MSME), banks prefer a certificate not older than 3–6 months.

If you are applying for multiple loans or schemes, you may need to get it reissued to match each lender’s requirement.

Always share updated documents with your CA so the certificate reflects your latest and accurate financial position.

Common Mistakes to Avoid While Applying for Net Worth Certificate

Submitting a Net Worth Certificate that has already expired — banks will not accept outdated documents.

Forgetting to list all assets or liabilities, which can make your net worth calculation incorrect.

Getting a certificate that is not signed and verified by a practicing CA, which makes it invalid for banks.

Not checking whether your CA has generated a valid UDIN, which is mandatory for authentication.

Having mismatches between your bank statements, financial statements, and the details in the certificate.

Giving approximate values instead of proper documents or proofs for your assets.

Not updating old information like sold property, closed loans, or changed investments.

Submitting incomplete documents, which delays the certificate and loan process.

Not reviewing the draft certificate before final issue, leading to errors.

Ignoring the bank’s specific format or requirements for the certificate.

Connect With Us for Assistance on Net Worth Certificate & Loans

If you need quick and professional help with getting your Net Worth Certificate or understanding the right loan requirements, our team is here to make the process easy for you. We guide you step-by-step, prepare accurate CA-certified documents, ensure proper UDIN compliance, and help you avoid common mistakes that delay loan approvals. Whether you’re applying for a personal loan, business loan, or government-backed scheme, we make sure your documentation is complete and compliant.

You can reach us anytime for fast assistance, smooth processing, and expert support from start to finish. Just visit networthcertificate.in or call/WhatsApp +91 97263 65820. We help you get your certificate prepared quickly and confidently, so your loan approval becomes faster and stress-free.